The basic principle

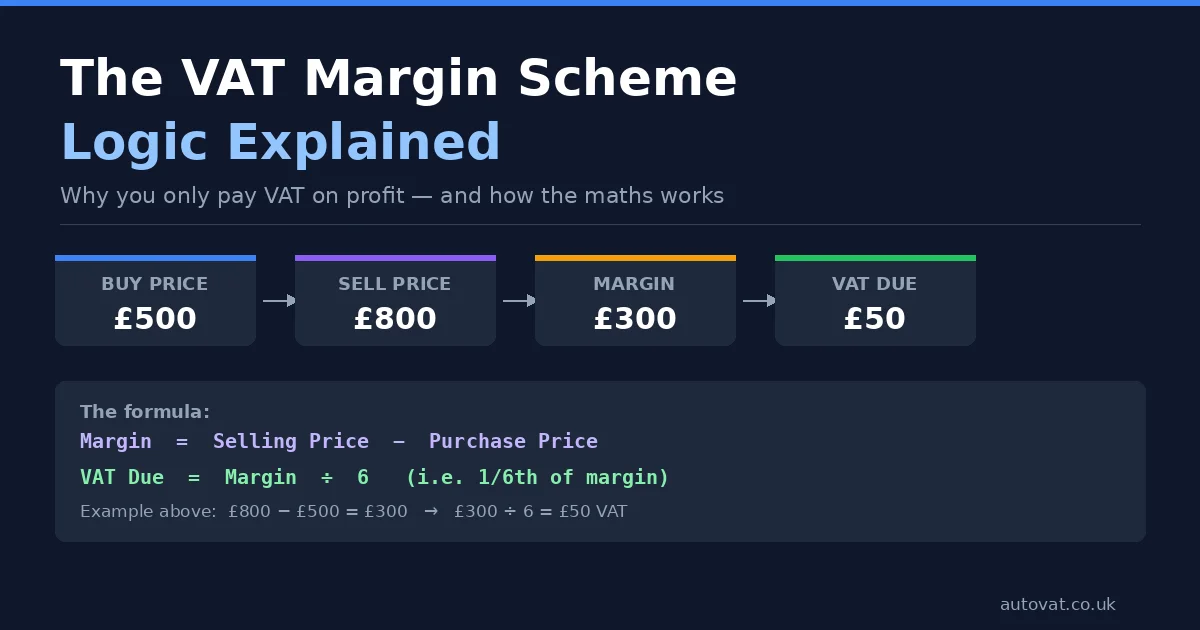

Under the VAT Margin Scheme, you pay VAT on the difference between what you paid for an item and what you sell it for — your profit margin. You do not charge VAT on the full selling price. The margin is treated as VAT-inclusive, meaning the VAT is already embedded within the margin rather than added on top.

This is an important distinction. Under standard VAT, if you quote a price of £1,000, you add 20% on top to get £1,200. Under the margin scheme, the margin itself already contains the VAT element, and you extract it using the VAT fraction.

The formula

The VAT fraction for the standard 20% rate is 1/6. To calculate the VAT due on a margin scheme sale:

Step 1: Calculate the margin — Selling price minus Purchase price

Step 2: Apply the VAT fraction — Margin × 1/6

If the margin is negative (you sold for less than you paid), no VAT is due on that item. Under individual item accounting, a loss on one item cannot be used to reduce the VAT owed on a profitable item from a different transaction.

The formula is confirmed in HMRC's VAT margin scheme guidance.

Worked examples

Example 1: A straightforward second-hand sale

You buy a second-hand watch from a private seller for £400. You sell it for £700.

- Margin = £700 − £400 = £300

- VAT = £300 × 1/6 = £50.00

You pay £50 VAT to HMRC. Your net profit on the sale is £300 − £50 = £250 (before other costs).

Example 2: A higher-value vehicle sale

You buy a used car for £8,500 from a private individual. You sell it for £12,000.

- Margin = £12,000 − £8,500 = £3,500

- VAT = £3,500 × 1/6 = £583.33

Example 3: A loss-making sale

You buy a piece of vintage furniture for £1,200 and sell it for £950.

- Margin = £950 − £1,200 = −£250 (a loss)

- VAT due = £0

No VAT is payable on this transaction. Under individual item accounting, the loss cannot be offset against profits on other items. Under global accounting, it can be offset within the same VAT period — see our guide to global vs individual accounting for more detail.

Example 4: A quarterly return with multiple items

Over one VAT quarter you sell five items:

- Item A: bought £200, sold £350 — margin £150

- Item B: bought £500, sold £750 — margin £250

- Item C: bought £300, sold £280 — margin −£20 (loss, zero VAT)

- Item D: bought £1,000, sold £1,600 — margin £600

- Item E: bought £150, sold £220 — margin £70

Total eligible margin = £150 + £250 + £0 + £600 + £70 = £1,070

Total VAT due = £1,070 × 1/6 = £178.33

A common mistake: applying 20% to the margin

A frequent error is to calculate VAT as 20% of the margin rather than using the 1/6 fraction. These give different results. 20% of £300 = £60. But 1/6 of £300 = £50. The 1/6 fraction is the correct method because the margin is treated as VAT-inclusive. Applying 20% on top would effectively be charging VAT on VAT. Always use the 1/6 fraction.

Use our VAT margin calculator

If you want to quickly check VAT on any margin scheme transaction, use our free VAT Margin Scheme Calculator. And if you want margin calculations handled automatically across all your stock without any manual arithmetic, get in touch to see how AutoVAT works.