How standard VAT works

Under standard VAT accounting, you charge 20% VAT on every sale you make. You collect that VAT from your customer and pay it to HMRC, minus any input VAT you have reclaimed on your business purchases. In a typical product business, you buy goods with VAT, reclaim that VAT as input tax, charge output VAT on the sale, and pay HMRC the difference.

For second-hand goods dealers, this creates a serious problem. Most second-hand stock is bought from private individuals, who cannot charge or provide a VAT invoice. So there is no input VAT to reclaim. Under standard VAT, you would charge 20% output VAT on the full selling price — even though you paid the full purchase price with no VAT offset. In most cases, that makes second-hand dealing economically unviable.

How the margin scheme works

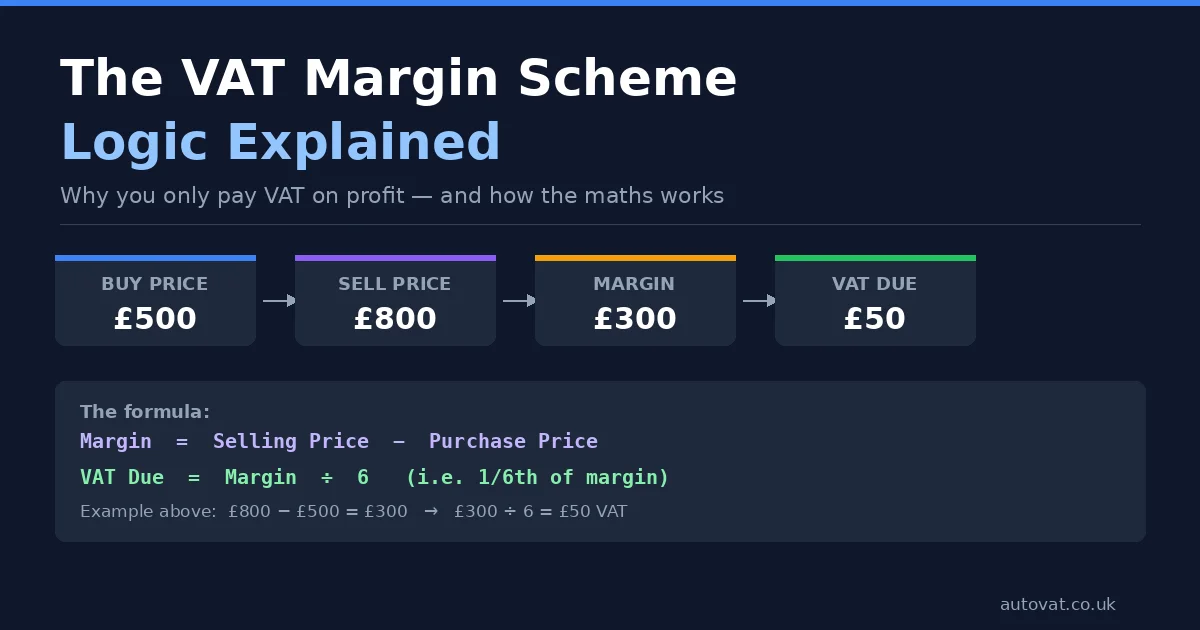

The VAT Margin Scheme solves this problem. Instead of charging VAT on the full selling price, you only pay VAT on your profit margin — the difference between what you paid and what you sell for. The VAT fraction applied to that margin is 1/6 (which is the VAT-inclusive rate for 20% VAT). So if you buy for £500 and sell for £800, your margin is £300 and VAT due is £300 × 1/6 = £50.

This reflects the economic reality far more accurately: VAT on the seller's value added, not on the full transaction value. Full details of how the scheme works are set out in HMRC's VAT margin scheme guidance.

Side-by-side comparison

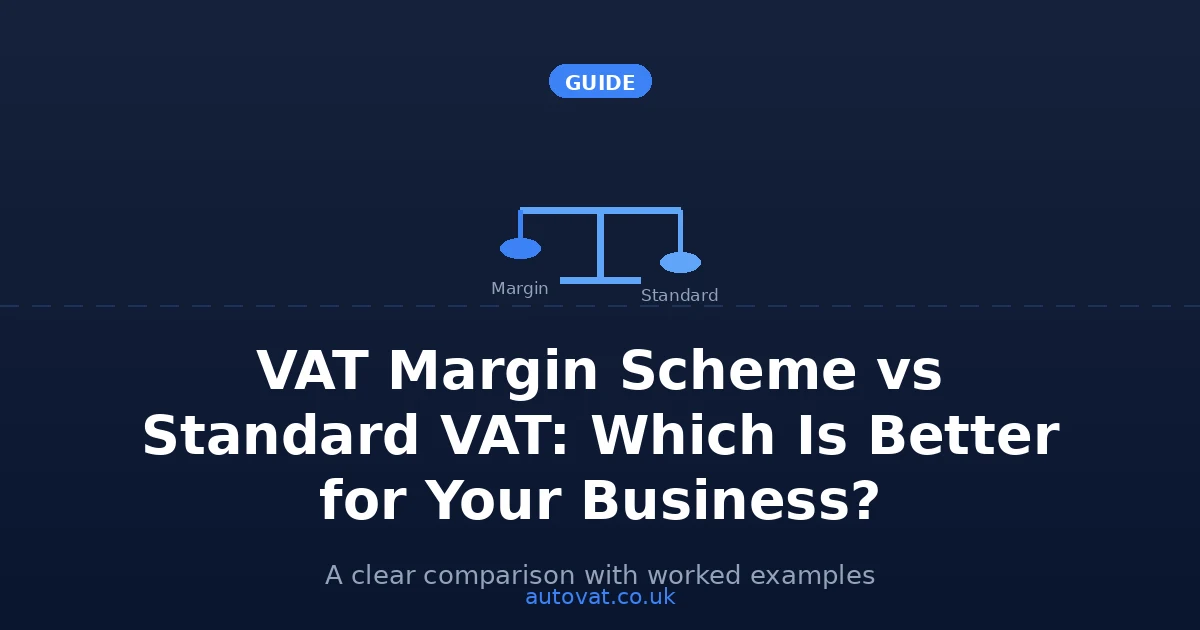

To make the difference concrete, here is an example using the same transaction under both methods:

You buy a second-hand camera from a private individual for £600 and sell it for £900.

Under standard VAT: You charge 20% VAT on £900. Output VAT = £150. Input VAT reclaimed = £0 (no VAT invoice from the private seller). Net VAT payable to HMRC = £150.

Under the margin scheme: Margin = £900 − £600 = £300. VAT = £300 × 1/6 = £50. Net VAT payable to HMRC = £50.

The margin scheme saves you £100 on this single transaction. Across hundreds of sales per year, the difference is substantial.

When does standard VAT make more sense?

The margin scheme is almost always better for dealers buying second-hand goods from private individuals. But there are situations where standard VAT accounting is preferable:

- You buy from VAT-registered businesses — if your supplier charges you VAT and you have a valid VAT invoice, you can reclaim that input VAT under standard accounting. The item is not eligible for the margin scheme in this case.

- You are selling new goods alongside second-hand — new goods cannot use the margin scheme. They must be accounted for under standard VAT rules. Mixed stock businesses often run both methods side by side.

- Your margins are very thin — if you routinely sell items for little more than you paid, the VAT saving from the margin scheme is small, and some dealers prefer the simplicity of standard VAT for low-margin lines.

You can mix both methods

It is perfectly legal to use the margin scheme for eligible second-hand goods and standard VAT for everything else. Many dealers do exactly this — margin scheme for stock bought from private individuals, standard VAT for new accessories or goods bought from VAT-registered suppliers. The key is to keep the two categories of stock clearly separated in your records.

Getting the choice right in practice

For the vast majority of second-hand goods dealers buying from private sellers, the margin scheme is the right choice. The VAT saving is real and consistent, and the record-keeping obligations — while more detailed than standard VAT — are manageable with the right software. AutoVAT handles the margin scheme accounting automatically so you get the VAT benefit without the administrative burden. Get in touch to find out how it works for your business, or estimate your savings with our free VAT Margin Scheme Calculator.