Start with the problem the scheme was designed to solve

To understand why the VAT Margin Scheme exists, you need to understand the unfairness it was designed to correct.

Standard VAT works well for new goods. A manufacturer makes something, adds 20% VAT when they sell it, the buyer pays that VAT, and the VAT flows to HMRC. Simple. But consider what happens with second-hand goods. A private individual buys a car for £10,000, pays £2,000 in VAT as part of that price. A few years later they sell it to a dealer for £6,000. No VAT on that private sale — private individuals cannot charge VAT. The dealer then sells it on for £7,500. Under standard VAT rules, the dealer would charge 20% VAT on the full £7,500, sending £1,250 to HMRC.

But there is a problem: that £7,500 car was already VAT-bearing when it was new. The original owner paid VAT on it. The dealer cannot reclaim that historical VAT because they bought it from a private individual who never charged it. If the dealer now pays VAT on the full selling price, VAT is being charged on the same underlying value twice — once when the item was new, and again every time it passes through a VAT-registered dealer's hands. That is double taxation, and it was making the second-hand trade economically unworkable.

The VAT Margin Scheme was HMRC's solution. Instead of charging VAT on the full selling price, the dealer only pays VAT on the profit margin — the new value they actually added. The logic is elegant: the existing value in the goods has already been VAT-bearing. Only the new value created by the dealer (buying low, selling higher, adding their expertise and effort) should attract fresh VAT.

The formula, step by step

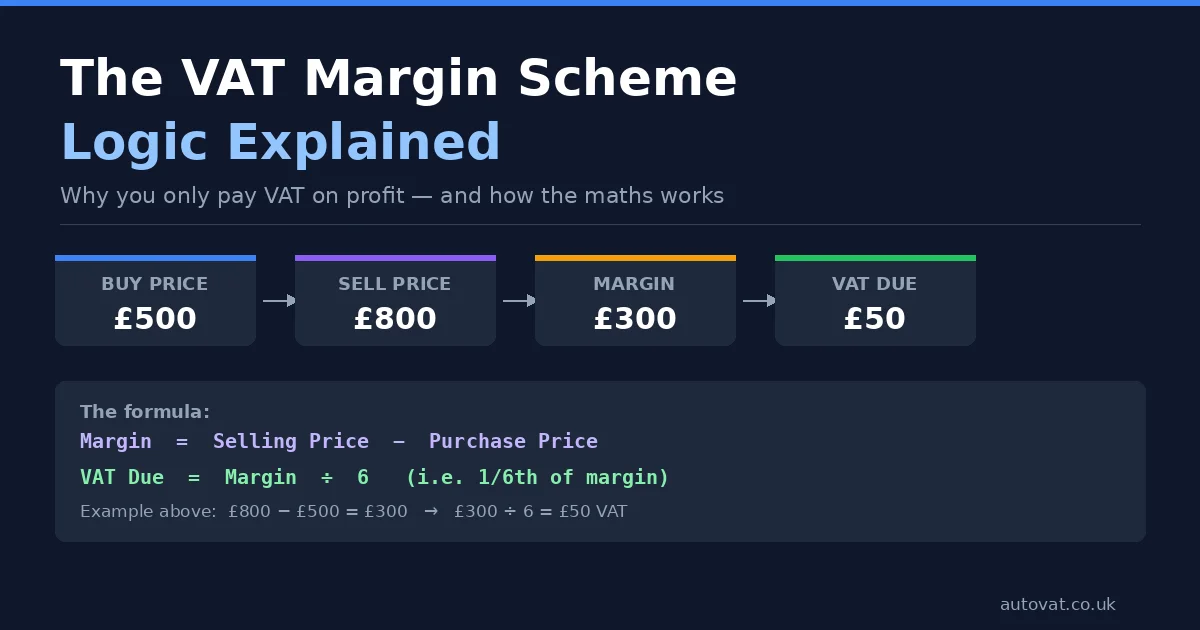

The Margin Scheme calculation has two steps and never changes regardless of what you are selling.

Step 1: Calculate your margin. Margin = Selling Price − Purchase Price. That is it. If you bought a piece of furniture for £400 and sold it for £650, your margin is £250.

Step 2: Calculate the VAT within that margin. VAT = Margin ÷ 6. So for a £250 margin: £250 ÷ 6 = £41.67 VAT due to HMRC.

The reason you divide by 6 rather than multiply by 20% is important and worth understanding. The VAT is already embedded within your selling price — it is part of the £650, not added on top of it. When VAT is included in a price and the rate is 20%, the VAT portion is one sixth of the total (because 20/120 = 1/6). You are extracting the VAT that is already inside the price, not adding new VAT on top.

This is the same maths used when a standard VAT-registered business works out the VAT element of a VAT-inclusive price. One sixth is always the fraction. Multiply by 20% is only correct when calculating VAT to add on top of a net price.

A worked example: second-hand car

You buy a used car at auction for £3,200. You spend nothing on repairs. You sell it through your forecourt for £4,500.

Margin: £4,500 − £3,200 = £1,300. VAT due: £1,300 ÷ 6 = £216.67.

Compare this to standard VAT on the full price: £4,500 × 20% = £900. The Margin Scheme saves you £683.33 in VAT on this single transaction. For a dealer turning over many cars a year, the cumulative saving is enormous — and is the entire reason the scheme exists.

Your customer pays £4,500 regardless of which VAT method you use. The difference is entirely in how much of that £4,500 you pass to HMRC versus keep as your revenue.

You can check the maths on any transaction with our free VAT Margin Scheme Calculator.

A worked example: antique item

You buy a Victorian writing desk at a house clearance for £180. You sell it at a fair for £420.

Margin: £420 − £180 = £240. VAT due: £240 ÷ 6 = £40.

Your net revenue after VAT: £420 − £40 = £380. Your gross profit before other costs: £380 − £180 = £200.

Under standard VAT, you would owe £70 (£420 × 1/6, since the price would be VAT-inclusive). The Margin Scheme saves you £30 here, and the saving scales with the ratio of your margin to your selling price — the lower your margin as a percentage of sale price, the more pronounced the benefit.

What happens when you sell at a loss or break even?

If your selling price equals or falls below your purchase price, your margin is zero or negative. VAT due is therefore zero. You owe HMRC nothing on that transaction.

This is one of the most important protections the scheme offers. Under standard VAT, you would owe VAT on the full selling price even when making a loss on the item. Under the Margin Scheme, no profit means no VAT — the tax tracks your actual economic position rather than your gross revenue.

The one thing you cannot do is use a loss on one item to reduce the VAT owed on another item you sold profitably in the same period — unless you are using global accounting, which is a separate method covered in its own article. Under individual accounting (the default), each item stands alone.

Why VAT cannot be shown separately on your invoices

This confuses many new dealers. Under standard VAT, invoices show the net price, the VAT amount, and the gross total as three separate figures. Under the Margin Scheme, you are not permitted to do this.

The reason comes directly from the logic of the scheme. The VAT is embedded within your selling price. It was never separately charged to the customer — they did not pay a net amount plus VAT. They just paid your price, and inside that price sits a fraction that you will pass to HMRC. If you showed a separate VAT figure, you would be implying that the customer paid that VAT and could potentially reclaim it. They cannot — the scheme prohibits input VAT recovery on Margin Scheme purchases. Showing a VAT figure would be misleading and non-compliant.

Instead, your invoices and receipts for Margin Scheme goods should simply show the total price and include the statement that the sale is made under the VAT Margin Scheme and that VAT cannot be reclaimed by the buyer. The exact wording HMRC recommends is: "VAT margin scheme — buyer cannot reclaim VAT."

What costs count as the purchase price?

Only the original acquisition cost of the item counts as the purchase price in the margin calculation. This is a common point of confusion.

If you buy a car for £3,000 and then spend £400 repairing it before resale, your purchase price for margin scheme purposes is still £3,000. The £400 repair cost is not deductible from your selling price within the scheme. Your margin is calculated on the original price only. The repair costs are business expenses you can deduct elsewhere for income or corporation tax purposes, but they do not affect your VAT margin calculation.

Similarly, auction fees, transport costs, valeting, advertising — none of these reduce your margin for VAT purposes. The formula is always just selling price minus original purchase price.

The stock book requirement

The Margin Scheme only works if HMRC can verify that you have correctly calculated the margin on every eligible item. This is why the scheme requires every dealer to maintain a stock book — a record that captures, for each item: a unique reference number, the purchase date, the purchase price, a description, the sale date, the sale price, the margin, and the VAT due.

Without a proper stock book, HMRC cannot confirm your margin calculations during an inspection. If your records are incomplete or missing, HMRC can disallow the scheme for your business and assess VAT on your full selling prices instead — a potentially catastrophic outcome for a dealer with high turnover. Keeping the stock book is not optional; it is the price of admission to the scheme's benefits.

Who can and cannot use the scheme

The scheme is available to VAT-registered dealers buying and reselling eligible second-hand goods. The key eligibility rules are that the goods must be second-hand (previously owned), they must have been bought from someone who did not charge VAT on the sale (typically a private individual, or a business selling goods from their own use), and the goods must be ones where the original purchase did not allow the buyer to reclaim input VAT.

Goods that cannot be sold under the scheme include anything where the dealer was charged VAT on the purchase and reclaimed it (because the VAT chain is unbroken and standard accounting applies), precious metals, investment gold, and certain other specific categories. Motor vehicles are eligible with some additional rules around part-exchange transactions.

The bottom line: a fair tax on added value

The VAT Margin Scheme is not a loophole or a special favour. It is a principled correction to a genuine problem of double taxation in second-hand markets. The logic is sound: tax the new value added, not the recycled value that already bore VAT when new. The maths is simple: margin divided by six. The administration is straightforward if you maintain your stock book from day one.

What makes the scheme feel complicated is not the underlying concept but the record-keeping burden at scale — tracking purchase prices, matching them to sale records, calculating margins across hundreds of transactions per quarter. That is the problem AutoVAT was built to solve.