What is the VAT Margin Scheme?

The VAT Margin Scheme is an HMRC scheme that allows dealers in second-hand goods to pay VAT only on their profit margin rather than on the full selling price. This is a significant saving — especially when buying and selling items where VAT was already paid by the original owner.

Who qualifies?

The scheme applies to businesses that buy and sell:

- Second-hand goods

- Works of art

- Antiques and collectors' items

You can use the scheme only for items you bought without paying VAT — typically from private individuals or other businesses using the margin scheme.

How is VAT calculated?

Instead of charging VAT on the full selling price, you calculate your margin (selling price minus buying price) and pay VAT on that amount at 1/6th of the margin (for the standard 20% rate).

Example: You buy a car for £5,000 and sell it for £7,000. Your margin is £2,000. VAT = £2,000 ÷ 6 = £333.33.

Why is record-keeping so important?

HMRC requires detailed records for every item bought and sold under the scheme. Each item needs a stock book entry with purchase price, sale price, margin, and VAT due. Missing records can mean you lose the right to use the scheme — and face backdated VAT bills on full selling prices.

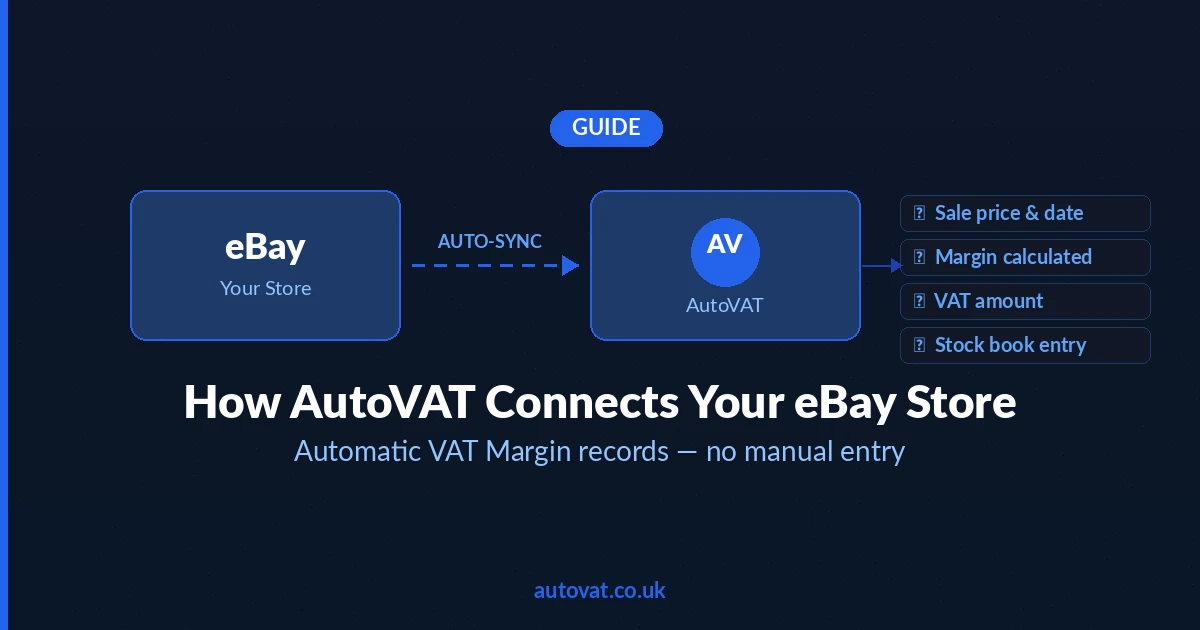

How AutoVAT helps

AutoVAT automates every part of this process — syncing your sales and purchases from eBay, Amazon, Shopify, and more, calculating margins automatically, and generating HMRC-ready reports at the click of a button. Want to quickly estimate your VAT on any deal? Use our free VAT Margin Scheme Calculator.