The core rule: it's one or the other

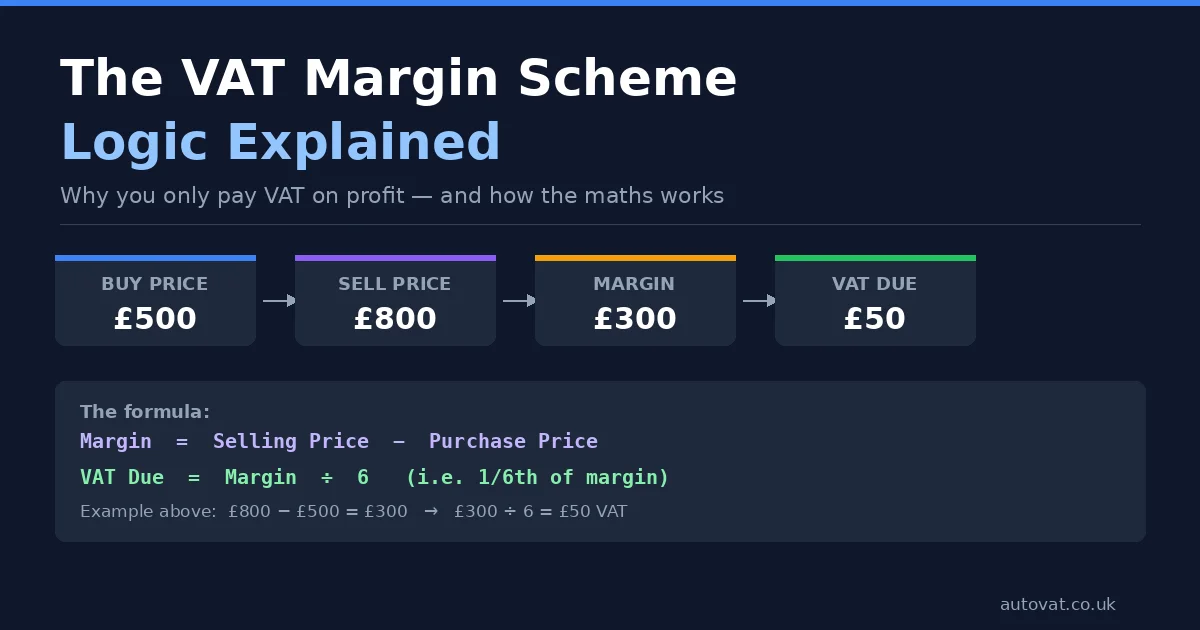

When you sell a stock item under the VAT Margin Scheme, you pay VAT on your profit margin — the difference between what you paid and what you sold it for. In return for that favourable treatment, HMRC does not allow you to reclaim any input VAT on costs directly associated with that item. This is a deliberate trade-off built into the scheme.

So if you buy a second-hand car for £3,000, spend £500 on an MOT and service (incurring £100 VAT on those repair costs), and then sell it for £5,000, you cannot reclaim that £100 VAT. You simply calculate your margin as £2,000 (selling price minus purchase price) and pay VAT on that.

This is confirmed in HMRC's VAT margin schemes guidance and VAT Notice 718.

What costs does this cover?

The restriction on input VAT reclaim applies to any cost that is directly connected to a margin scheme item, including:

- Mechanical repairs or servicing (common for vehicle dealers)

- Cleaning, valeting, or reconditioning

- Restoration work on antiques or furniture

- Testing, calibrating, or refurbishing electronics

- Parts fitted to the item

All of these are treated as part of your cost of sale. You bear the VAT on them as part of running your business, but you cannot offset it against your VAT bill the way you would with standard overhead costs.

What about general business overheads?

This is where dealers sometimes get confused. The input VAT restriction only covers costs that are directly related to specific margin scheme items. General business overheads — rent, utilities, general office supplies, accountancy fees — are not caught by this rule. You can still reclaim input VAT on those in the normal way on your VAT return.

The distinction is whether a cost relates to a specific eligible item or to your business as a whole. A valeting bill for a specific car: not reclaimable. Your monthly workshop rent: reclaimable as normal.

Does this make the margin scheme less worthwhile?

For most dealers in second-hand goods, no — the margin scheme still works out significantly better than standard VAT accounting. Under standard VAT, you would pay output VAT on the full selling price of every item. The margin scheme caps your VAT exposure to just the profit. Even accounting for the lost input VAT on repair costs, you almost always pay less total VAT under the margin scheme.

The maths does change if you spend heavily on repairs relative to your margin. If you buy a vehicle for £5,000, spend £2,000 refurbishing it, and sell it for £7,500, your gross profit is only £500 — but you have borne significant repair VAT that you cannot reclaim. In situations like that, it can be worth getting advice on whether a particular item is worth keeping in the margin scheme or whether you would be better off treating it under standard VAT rules instead.

Getting the accounting right

The key is to keep repair costs clearly separated in your records — both for the items themselves and for general overheads. AutoVAT helps you track repair and reconditioning costs against specific stock items so your margin calculations are accurate, and flags which costs can and cannot be claimed on your VAT return. Get in touch to see how we can build this into your workflow.