Mistake 1: Mixing margin and standard-rated stock

Not all second-hand goods qualify for the margin scheme. If you buy an item from a VAT-registered business that charges you VAT, you cannot use the margin scheme for that item. Mixing eligible and ineligible stock is one of the most common mistakes dealers make.

Mistake 2: Poor or incomplete stock records

HMRC requires a stock book for every item. Many dealers keep records on spreadsheets or paper — which are easy to lose, damage, or make errors in. A missing record means you may have to pay VAT on the full selling price for that item.

Mistake 3: Calculating VAT on the full price

Some dealers accidentally add VAT at 20% on the full selling price rather than on the margin. The correct rate is 1/6th of the margin (which equates to 20% of the margin). Overcharging VAT to customers and paying too much to HMRC erodes your profit unnecessarily.

Mistake 4: Including repair and restoration costs in the margin calculation

You cannot add repair costs to your purchase price to reduce the margin. HMRC is clear: only the original purchase price counts. Any costs you add that aren't the original purchase price are not allowable.

Mistake 5: Not keeping records long enough

HMRC can investigate VAT records going back six years. Many dealers destroy records after a year or two — leaving them exposed to penalties and backdated assessments.

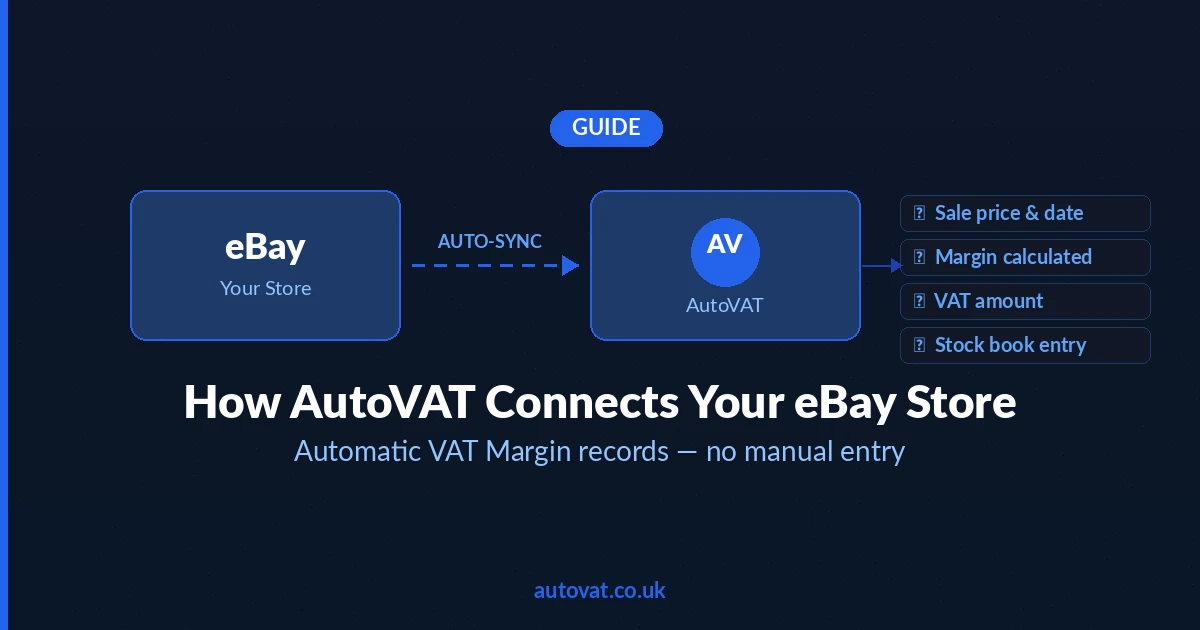

The easy fix

AutoVAT keeps compliant, permanent records for every item you buy and sell — organised, searchable, and exportable for your accountant at any time.