Why electronics resellers need to understand this

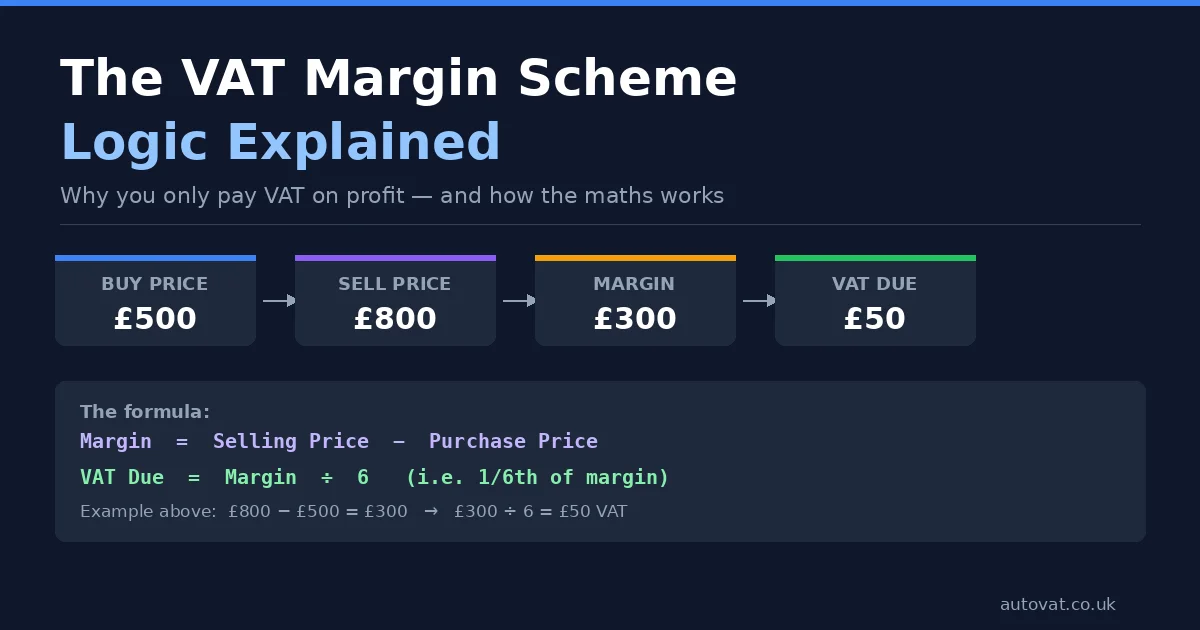

Electronics are high-value, fast-depreciating goods. A smartphone bought for £800 when new might change hands a year later for £400, then again for £300, and so on. At every stage where a VAT-registered dealer is involved, VAT applies to the transaction. Under standard VAT, a dealer buying a used phone for £250 and selling it for £320 would owe £53.33 in VAT on the full selling price — leaving a genuine profit of only £16.67 after VAT.

Under the VAT Margin Scheme, the same dealer would owe VAT only on the £70 margin: £70 ÷ 6 = £11.67. Their profit after VAT becomes £58.33 — more than three times higher. For dealers operating on thin margins across hundreds of transactions a month, this difference is the viability of the business.

What electronics qualify for the Margin Scheme

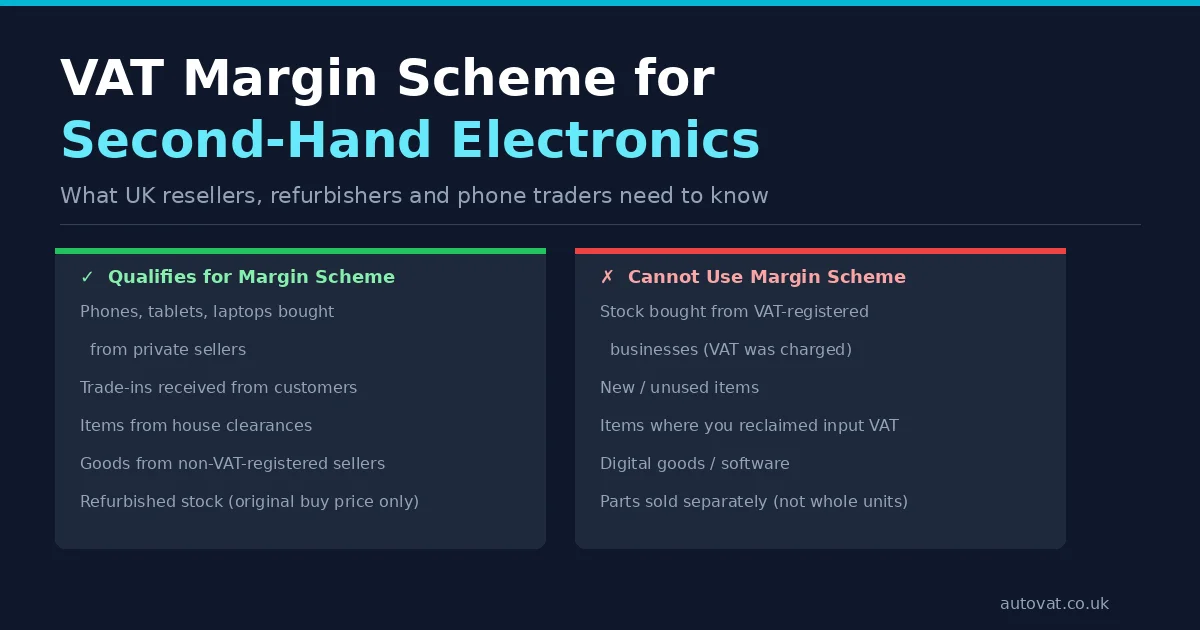

The Margin Scheme applies to second-hand goods that were previously owned and used, purchased from a seller who either did not charge VAT on the sale or was not VAT-registered. For electronics, this typically means items bought from private individuals — phones, tablets, laptops, cameras, gaming consoles, audio equipment, smartwatches, and similar consumer electronics.

The most common qualifying sources are private sellers on platforms like Facebook Marketplace, Gumtree, or local classified ads; trade-ins or part-exchanges accepted directly from customers; items purchased at car boot sales, house clearances, or charity sales; and goods bought from other small sellers who are not VAT-registered.

The defining rule is that the VAT chain must have been broken before you acquired the item. The original buyer paid VAT when the device was new. If it then passed through private hands — where no VAT was charged — and you buy it from that private person, the VAT chain is broken and the Margin Scheme applies.

What electronics do not qualify

If you buy second-hand electronics from a VAT-registered business that charges you VAT on the sale, the goods do not qualify for the Margin Scheme. This is because the VAT chain is unbroken — VAT was charged to you on the purchase, and you can reclaim it as input VAT. Standard VAT accounting then applies to your onward sale.

This catches out many electronics resellers who buy stock from trade suppliers, wholesalers, or other VAT-registered dealers. If your supplier's invoice shows a VAT amount and you reclaim that VAT, you cannot then use the Margin Scheme when you sell the item. You must account for VAT on the full selling price instead.

Brand new or unused items are similarly ineligible — the Margin Scheme is for second-hand goods only. A phone that was never activated or opened does not qualify even if it was technically "owned" by a private individual.

Refurbished electronics: the repair cost trap

Many electronics resellers buy broken or damaged devices cheaply, repair them, and sell them at a higher price. This is a legitimate and often profitable business model — but there is a VAT trap that catches people out.

When you buy a cracked-screen iPhone for £80 and spend £60 on a screen replacement, your total cost is £140. You sell the repaired phone for £220. It is tempting to calculate your margin as £220 − £140 = £80, and pay VAT of £13.33. But HMRC does not allow this.

Under the Margin Scheme, only the original purchase price of the item counts in the margin calculation. Repair costs, replacement parts, cleaning materials, accessories you add — none of these reduce the selling price for VAT purposes. Your margin is calculated as £220 − £80 = £140, giving VAT of £23.33.

The repair costs are still deductible as a business expense for income or corporation tax, but they do not affect your VAT Margin Scheme calculation. This is one of the most common misunderstandings in electronics reselling and can lead to significant VAT underpayment if not handled correctly.

There is a further complication with repair parts: if you buy a replacement screen from a VAT-registered supplier, you pay VAT on that purchase. You can reclaim that input VAT as a normal business cost — but that VAT recovery does not interact with the Margin Scheme calculation on the device itself.

Trade-ins and part-exchanges

Many electronics retailers accept trade-ins — a customer brings in their old phone as part-payment for a new or different device. The used device received as a trade-in qualifies for the Margin Scheme when you later resell it, provided the customer was a private individual and no VAT was charged on the trade-in transaction.

The purchase price for Margin Scheme purposes is the value you assigned to the trade-in at the time of the transaction — the amount you effectively paid for it by crediting it against the customer's purchase. This figure needs to be recorded in your stock book at the time of the trade-in, not reconstructed later.

If the trade-in comes from a VAT-registered business (for example, a company trading in its old laptops), you will likely be charged VAT on the value of the goods handed over, making Margin Scheme treatment unavailable for those items.

Bundles and accessories

Electronics resellers frequently sell items with accessories — a laptop with a charger and case, a phone with earbuds and a screen protector, a camera with a bag and memory cards. How you handle bundles affects your VAT position.

If all items in the bundle were bought together as a single lot from a private seller and you sell them together as a single unit, the Margin Scheme applies to the bundle as a whole. Your purchase price is what you paid for the lot, your selling price is what you receive, and the margin is the difference.

If the main item qualifies for the Margin Scheme but the accessories are new items you purchased separately from a VAT-registered supplier, those accessories should be accounted for separately under standard VAT. Mixing them into a Margin Scheme calculation would incorrectly reduce your VAT liability.

The practical approach is to sell the eligible second-hand item and any new accessories as separate line items, with the device under Margin Scheme and the new accessories under standard VAT. This keeps your records clean and your VAT position correct.

Selling on eBay, Amazon and other platforms

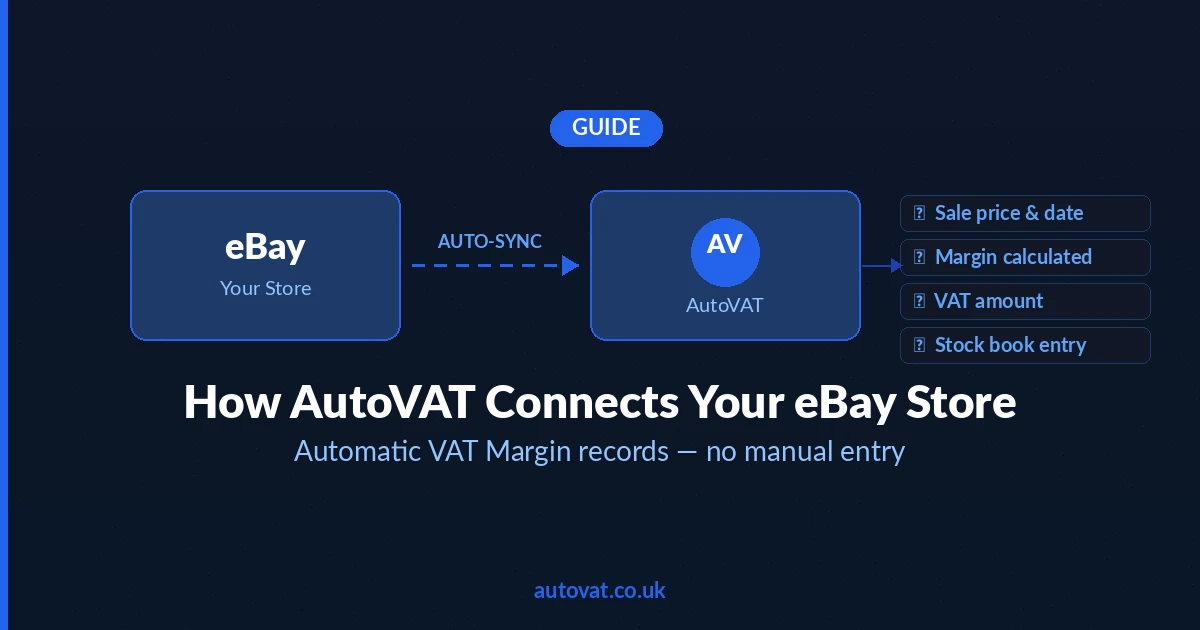

Most second-hand electronics dealers sell through online marketplaces. The platform handles the transaction, but the VAT accounting remains entirely your responsibility — eBay and Amazon do not know whether a particular listing falls under the Margin Scheme or standard VAT.

For eBay sellers, the key practical challenge is connecting each completed sale in your eBay order history to the corresponding purchase record in your stock book. If you sell 50 items a week, doing this manually is time-consuming and error-prone. A system that links your eBay order data to stock purchase records — whether a well-maintained spreadsheet or dedicated software like AutoVAT — is essential for staying on top of this at volume.

From a customer-facing perspective, your eBay listings and invoices should not show a separate VAT amount for Margin Scheme items. The price you advertise is the price the buyer pays, and the VAT is embedded within that price and accounted for in your own records.

Mixing Margin Scheme and standard-rated stock

If you sell both eligible second-hand electronics (Margin Scheme) and new accessories or items bought from VAT-registered suppliers (standard VAT), you need to maintain completely separate records for each category. HMRC requires clear separation — you cannot blend Margin Scheme and standard VAT items into a single calculation.

On your quarterly VAT return, the figures from both streams feed into the same return boxes, but your underlying records must clearly show which sales were Margin Scheme and which were standard-rated. During an HMRC inspection, an inspector will want to see that separation clearly demonstrated.

Record-keeping for electronics dealers

HMRC requires a stock book for every item sold under the Margin Scheme. For electronics, a good stock book entry includes: a unique stock reference number (for example, a sequential number or the device's IMEI or serial number), the date of purchase, the purchase price paid, a description of the item including make, model and condition, the date of sale, and the selling price. The margin and VAT due should also be recorded.

Using the device's serial number or IMEI as the stock reference has a practical advantage: it provides an unambiguous link between the physical item, your purchase record, and your sale record, which is exactly what HMRC wants to see if they inspect your books.

The bottom line for electronics resellers

The VAT Margin Scheme can make a decisive difference to the profitability of a second-hand electronics business, particularly in a market where margins are already thin due to competition. The eligibility rules are not complicated once you understand the core principle — the VAT chain must have been broken before you acquired the item. The practical challenges are in maintaining clean records across high volumes of transactions and keeping Margin Scheme stock clearly separated from any standard-rated stock.

AutoVAT is built for exactly this kind of business — connecting your sales data to a compliant stock book, calculating the correct VAT on every transaction, and keeping the records that HMRC requires, so you are never scrambling at quarter end.