Note: Tax deadlines and rules can change. Always verify dates directly with HMRC at gov.uk or with a qualified accountant before acting. This article reflects the position as of May 2026.

Why deadlines matter more than people realise

HMRC's penalty system is unforgiving by design. A Self Assessment return filed one day late triggers an automatic £100 fine — regardless of whether you owe any tax. Corporation Tax paid a day after it is due starts accruing daily interest. VAT returns submitted late accumulate penalty points under the new regime introduced in 2023, and once you hit the threshold, fixed financial penalties apply.

The good news is that every deadline in this article is known well in advance. There is no reason to be caught out — and with a clear calendar view of what is due and when, staying compliant is a straightforward planning exercise.

Self Assessment deadlines for the 2025/26 tax year

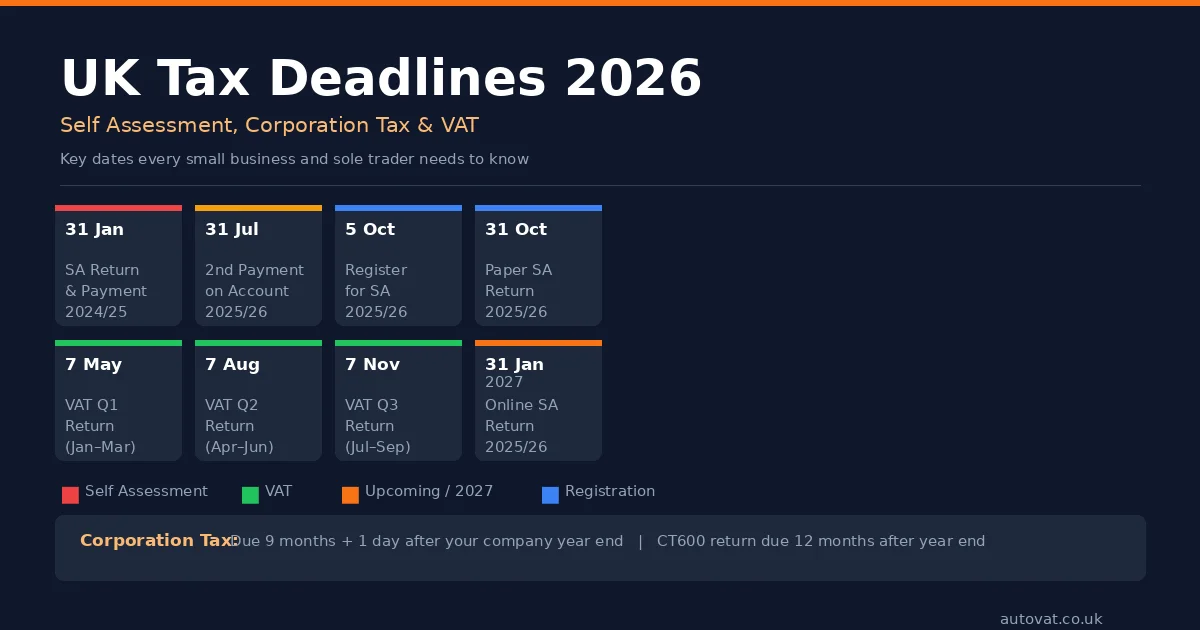

The UK tax year runs from 6 April to 5 April. The 2025/26 tax year ended on 5 April 2026. The following dates now apply for filing and payment.

5 October 2026 — Register for Self Assessment if you have not filed before and you need to file a return for 2025/26. This applies if you became self-employed, started receiving rental income, or had other untaxed income in the 2025/26 tax year. Missing this date does not create an immediate penalty, but leaving it later reduces your time to gather records before the filing deadline.

31 October 2026 — Paper Self Assessment return deadline for the 2025/26 tax year. If you prefer to file a paper return rather than online, this is your deadline. Very few people file on paper now — the online system is faster, more convenient, and gives you until January.

30 December 2026 — Opt into PAYE collection if you owe less than £3,000 in tax and want HMRC to collect it through your tax code rather than as a lump sum payment in January. You must file your online return by this date to qualify for this option.

31 January 2027 — Online Self Assessment return deadline for the 2025/26 tax year. This is the main deadline most people work to. Your completed return must be submitted online by midnight on 31 January 2027. Late filing triggers an automatic £100 penalty, rising to £10 per day after three months, and then further fixed penalties at six and twelve months.

31 January 2027 — Balancing payment due for any tax owed for 2025/26 that has not already been covered by payments on account. This is paid at the same time as your return is filed.

31 January 2027 — First payment on account for the 2026/27 tax year, if your Self Assessment liability exceeds £1,000. Payments on account are advance payments towards next year's tax bill, each equal to half your previous year's liability.

Payment on account dates for 2026

If your Self Assessment tax bill for 2024/25 exceeded £1,000, you will be making payments on account towards your 2025/26 liability. These are split into two instalments.

31 January 2026 — First payment on account for 2025/26. This date has already passed. If you missed it, interest will be accruing on the unpaid amount from that date.

31 July 2026 — Second payment on account for 2025/26. This is the next significant Self Assessment date for most sole traders and self-employed people. It equals half your 2024/25 tax liability. If your 2025/26 income will be significantly lower than 2024/25, you can apply to reduce your payments on account — but this must be done before the payment date.

Corporation Tax deadlines

Unlike Self Assessment, Corporation Tax deadlines are not fixed calendar dates — they are tied to each company's own accounting year end, which varies from company to company.

Corporation Tax payment is due 9 months and 1 day after your company's accounting year end. For a company with a 31 March 2026 year end, Corporation Tax is due by 1 January 2027. For a 31 December 2025 year end, it was due by 1 October 2026. Small companies (with profits below £1.5 million) pay in a single instalment. Larger companies pay in quarterly instalments — if this applies to you, you will already know.

CT600 Corporation Tax return must be filed with HMRC within 12 months of your accounting year end. For a 31 March 2026 year end, the deadline is 31 March 2027. Note that the payment deadline comes before the filing deadline — you must estimate and pay your tax before you have filed the return. Late payment triggers interest from the due date, and late filing of the CT600 produces a £100 automatic penalty.

Annual accounts at Companies House are due 9 months after your accounting year end for private limited companies (the same date as your Corporation Tax payment, roughly speaking). Late accounts filing at Companies House attracts automatic penalties starting at £150 for one day late and rising steeply.

Confirmation statement must be filed at Companies House once a year, within 14 days of the anniversary of your company's incorporation or your last confirmation statement. The fee is £34 online. This is separate from your accounts and easy to overlook — set a calendar reminder.

VAT deadlines for 2026

VAT-registered businesses must file a VAT return and pay any VAT due after every VAT period — usually quarterly. The deadline is one calendar month and seven days after the end of each VAT period. Under Making Tax Digital, returns must be filed using MTD-compatible software.

For businesses on the standard calendar quarters (periods ending March, June, September, December), the 2026 deadlines are as follows.

7 May 2026 — VAT return and payment for the January–March 2026 quarter. This date falls very shortly after the time of writing for many businesses.

7 August 2026 — VAT return and payment for the April–June 2026 quarter.

7 November 2026 — VAT return and payment for the July–September 2026 quarter.

7 February 2027 — VAT return and payment for the October–December 2026 quarter.

Your VAT periods may differ if your quarters end in different months. Check your VAT registration certificate or your HMRC online account if you are unsure when your periods end.

Under HMRC's penalty points system introduced in January 2023, each late VAT return submission earns one penalty point. Once you accumulate enough points (two for annual filers, four for quarterly filers), a £200 fixed penalty applies for each subsequent late return, and further penalties apply for late payment. Points expire after 24 months of compliance.

VAT Margin Scheme and quarterly deadlines

For dealers using the VAT Margin Scheme, the VAT return deadlines are the same as for any other VAT-registered business. What differs is what goes into the return — specifically Box 1, which should reflect the output VAT calculated on your margins rather than on your full selling prices.

The quarterly deadline is also the natural forcing function for keeping your stock book up to date. Every eligible item sold in the quarter needs to be in your stock book with its purchase price, selling price, margin, and VAT calculated before you can complete the return accurately. Dealers who let their stock book fall behind often find themselves scrambling in the days before the filing deadline — a source of both stress and errors.

Setting aside time at the end of each month to reconcile your stock book means the quarter-end is a simple totalling exercise rather than a reconstruction from scratch.

PAYE and payroll deadlines

If you employ staff, PAYE deadlines run monthly. PAYE and National Insurance contributions deducted from employees must be paid to HMRC by the 19th of the following month (22nd if paying electronically). Real Time Information (RTI) payroll submissions must be made on or before each pay day. Employer's National Insurance contributions are due at the same time as employee deductions.

The annual P60 must be given to all employees by 31 May each year — so for 2025/26, the deadline is 31 May 2026. The P11D reporting benefits in kind is due by 6 July 2026 for the 2025/26 tax year.

A practical approach to never missing a deadline

The most effective thing any small business owner can do is put every relevant deadline into their calendar at the start of each year with a two-week advance reminder. Most penalties are entirely avoidable — HMRC does not give discretion for simply forgetting a date, but it cannot charge you for a return filed on time.

For VAT in particular, the combination of quarterly deadlines, Making Tax Digital requirements, and Margin Scheme calculations creates a regular administrative burden. Software that automates the record-keeping and produces the correct VAT figures for each return removes the bulk of that burden — leaving only the actual submission, which takes minutes.